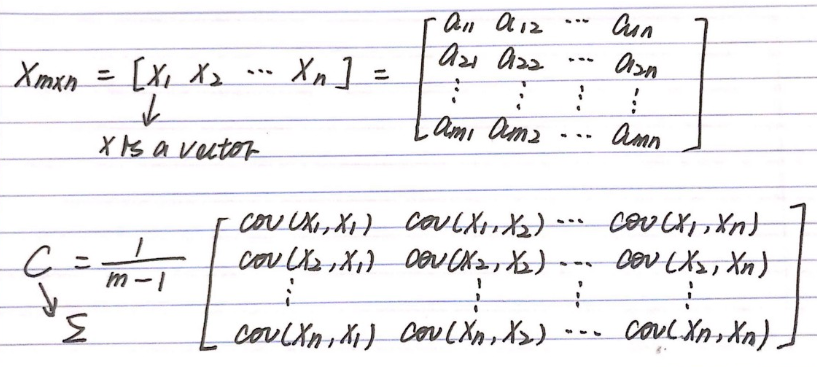

In probability theory and statistics, a covariance matrix, also known as auto-covariance matrix, dispersion matrix, variance matrix, or variance–covariance matrix, is a matrix whose element in the i, j position is the covariance between the i-th and j-th elements of a random vector.

en.wikipedia.org/wiki/Covariance_matrix

Covariance measures how much two random variables vary together in a population.

When the population contains higher dimensions or more random variables, a matrix is used to describe the relationship between different dimensions.

In a more easy-to-understand way, covariance matrix is to define the relationship in the entire dimensions as the relationships between every two random variables.

Yitong Ren - «The significance and applications of covariance matrix» (2019-05-01)